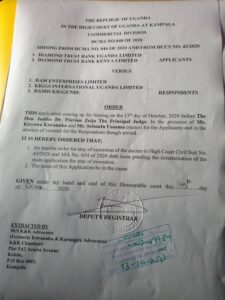

KAMPALA: Businessman Ham Kiggundu’s celebrations have dealt a blow as Court on Tuesday issued an interim order for stay of execution of the decree in High Court Suit No.43/2020 and Miscellaneous Application No.654 of 2020, pending the determination of the main case where Kiggundu and his companies Ham Enterprises Limited and Kiggs International Uganda Limited sued Diamond Trust Bank Uganda and Diamond Trust Bank Kenya for allegedly deducting Shs120 billion from his account bank account without his knowledge.

The Principal Judge, Justice Dr. Flavian Zeija delivered the interim order on Wednesday in the presence of M/S K & K Advocates, the lawyers for Diamond Trust Bank Uganda and Diamond Trust Bank Kenya, even though Kiggundu’s lawyers didn’t attend the reading of the interim order, much as they were served.

The latest development shames Kiggundu and his lawyers who were last Wednesday favoured by Judge Henry Peter Adonyo who ruled that it was illegal for Diamond Trust Bank Uganda and Diamond Trust Bank Kenya to arrange a syndicated loan to Ham Enterprises, saying that it contravened the Financial Institutions Act, 2004.

The ruling last unsettled the local banking industry, forcing all chief executive officers of 35 banks and other financial institutions to protest against the ruling that implied the syndicated loans are illegal in Uganda.

The two affiliated commercial banks availed over Shs39.7 billion for Ham Enterprises but has defaulted on paying back the loans. Kiggundu acquired the loans in four tranches; US$6.2 million, US3.2 million, US$458, 604 and Shs2.8 billion from Diamond Trust Bank Uganda and Diamond Trust Bank Kenya. The loans were consolidated later over two years ago and were to run from five years, ending August 23, 2023.

Instead Kiggundu turned around to sue Diamond Trust Bank Uganda for fraud, alleging that the bank has been deducting his money from his bank accounts to the tune of Shs120 billion. His claim was based on his own private audit of the bank accounts, which was contested by the banks and instead Judge Adonyo ordered for an independent audit, but he would later accept kiggundu’s application to have the independent audit halted on grounds that the businessman had to validate the loans given to him at the time he needed the money most.

The Ministry of Finance came out after the ruling saying that they were discussing with international lenders, development partners and private sector players to address the matter. BoU have come out to say that they are waiting to go through the detailed written ruling to respond appropriately. Chief executive officers of all commercial banks in the country are scared by the ruling that outlaws syndicated loans which they say stand at a tune of about Shs5.7 trillion, minus other monies that were being arranged to arrive in the country for use. If that happened, they cry, it would be a disaster for the local banking industry and the Ugandan economy at large.

Legal expert view of syndicated loans

A legal expert who has written about syndicated loans says the case should not have finally determined at the preliminary application level as there were other considerations to be made.

The short formulation, according to the expert, is that the court applies the system of law with which the contract has the closest and most substantial connection. “The question then becomes, which transaction and what are the circumstances of the case?”

He says Ham Enterprises Ltd v DTB case had six key connections:

- the lender was in Kenya,

- the loan contract was made in Kenya,

- the location of the debt (situs) was Kenya;

- the mortgaged property was in Uganda and the registration of the securities happened in Uganda,

- the collection agent was in Uganda;

- the borrower was in Uganda.

still, he says, there are some generally agreed principles. First, he says, the solution adopted by the court should encourage the economic and social development of the country. “That is usually achieved by promoting certainty in commercial transactions, and in turn, respecting the expressed intentions of the parties. Where there is no express choice, the court should not disappoint the parties and should apply a system of law that preserves the contract, rather than striking it down. In other words, the court should endeavour to hold the contract as valid because that is the presumed intention of the parties.”

He further says that: “Without the benefit of knowing what the parties expressly agreed upon and, therefore, what was documented in the choice of law and choice of jurisdiction clause in the Ham Enterprises Ltd v DTB case, and without any evidence displacing the general approaches to the subject, the case was governed by Kenyan law and should have been decided by the appropriate court for the Kenyan city where the loan was made. Further, on this analysis, the court should have been disinclined to apply Ugandan law since that application resulted in the loan contract being declared invalid.”

“To add a qualification to the above, that there will readily be a case where the cross-border lender (DTB (K)) accepts the law and jurisdiction of the borrower (Uganda) for ease of access to, and enforcement of, the security in the borrower’s jurisdiction. This possibility cannot be ruled out in the instant case since the borrower’s relationship bank was DTB (Uganda), the borrower’s counsel were in Uganda, and, to buttress those two elements, the legal systems of Uganda and Kenya are similar.”

He says that some information was not considered by Judge Adonyo. “Regardless of one’s preferred analysis, it is evident that some crucial information was not considered by the court and that this was a complex matter that required a detailed consideration by delving into the merits of the case.”