KAMPALA: Why do Ugandans come to banks rich with properties they pledge as securities and leave poor? Does it imply that all Ugandans are poor business Managers? Or the problem is with the System?

My arguments on the call for banking reforms in Sunday vision on August 16th , 2020 were specifically based on facts, reality within realistic current prevailing circumstances in our Banking sector today not written economic foreign principals or policies in line with the executive director of Uganda Bankers Association arguments.

Basing on realistic circumstances on ground, I identified hindering factors in our Banking sector which included the following;

Dominance by foreigners in top management position, current discriminative policies against Ugandans on Interest rates as we are given higher rates compared to foreigners, discrimination on Loan amounts disbursed as Ugandan are under Financed compared to foreigners, lack of transparency of Banks to customers, inadequate legal frame work and structures when it comes to Banking laws that tend to protect these Banks at the cost of we their customers.

Case in point is the Regulation 13 of the Mortgage act 2012 that tends to require a customer to deposit 30% of any disputed amount with the Bank before courts can proceed to hear their case which is contrary, repugnant and inconsistent to article 28 of the constitution that provide the right to fair hearing and access to courts of Law and article 26 which provides the right to property. Banks equally operate within our deposit and savings as capital yet repatriate all the profits depriving the country of it’s would be developmental capital among others.

The major factor in my submission was reason and reality which is equally the gap between success and failure let it be at an individual level, sector level like Banking or at national level. Most highly educated people are limited to thinking, never stretching up to reason. We think to survive but reason towards prosperity. Thinking is basic but reasoning is deep. Most highly educated people don’t think behold mere written principles or policies.

Thinking is a mere thought and attracts quick reactions at impulse where one may not give themselves a chance to understand something before they react but reasoning requires deep critical analysis of facts before you within realistic perimeters to achieve absolute total understanding of whatever is put before you then react. Reason helps one understand a problem thus giving them the ability to forge the right ample solution to such a problem. Inability to apply reason in all we do is the major frustrating factor that has hindered development of Uganda and Africa as a continent at large.

Equality is an element of reason so I can’t raise a problem of discrimination against Ugandans by foreign Banks and you discuss elaboratively current existing policies and structures reason looks at substance not formation or processes, discuss the raised problems in line with providing possible reasonable solutions rather than being defensive a fact that realistically exposes the truth that the raised defects in the Banking sector are true. Uganda Bankers Association and the entire Banking sector must approach these issues with soft hearts, pure clean hands and open minded rather than being simply defensive because the call for reforms was raised with clean intentions in the interest of developing our motherland Uganda.

The ED of Uganda Bankers Association tries to highlight the role played by the different players within the financial sector in general and specifically the role played by the commercial banks in the financial sector.

The article goes on to explain the board, executive, management and staff composition of banks at those different levels. And this is not where the problem is, because all these are paid or remunerated positions, (yes including boards of directors)

The boards of directors for example are appointed by the Real owners of the banks (foreign or local), and for those banks which are listed on the Uganda Securities Exchange (USE), the board is voted in by the shareholders who also usually control a small percentage with the biggest control going to the largest shareholders who are usually foreign based investors (individual or company).

So this is where the concern is, that the owners/largest shareholders of these banks have the final say or control on their bottom-line which is the Profit. They decide what happens and where the profits will be repatriated to; usually in their home countries. Therefore it is not just a matter of having indigenous Ugandans in positions of influence in these banks like the boards of directors, Chief Executives, senior management etc, when they have little control on the huge profits which are all made from and in Uganda!

The concern based suggestion here is that we need to have more of the locally OWNED commercial banks not just locally MANAGED.

Actually one of the major problems of the majority of our formal sectors in Uganda not just limited to Banking is that our decision makers are mainly highly educated people limited to knowledge never wisdom. They always hold a lot information having read so many books but with absolute inability to practically apply such knowledge within realistic and reasonable prevailing circumstances towards actual prosperity

We can’t find solutions to the problem at hand because we have failed to give ourselves a chance to adjust our mindset and understand the problems in totality. Yet the future of our dear country Uganda lies in the hands of our current generation.

My opinion based on reason is, the development of Uganda and transformation of the banking sector is an obligation we must accept at heart as Ugandans and stop discussing foreign economic policies that don’t fit within our social and current realistic prevailing circumstances. That’s why equity imputes an intention to fulfil an obligation.

Majority of your customers in the informal sector like those downtown and operating in markets don’t need lectures on how the Banking system works. They are the system themselves but rather require solutions to the day to day problems of the system raised above.

The problems raised above have held Ugandans at a disadvantage when it comes to individual progress and national development as they require reasonable soft flexible loans to invest in the development of long term projects like factories and industries to create a fundamental economic base for collective development.

Government has to rescue Ugandans from this poor current Banking structure through reforms because it’s only getting worse. The reaction of Uganda Bankers association (UBA) has only worsened our worry on Banks as its now evident that they propose to take over the mediation and arbitration procedures within the legal framework through (ICAMEK) so that Banks are the aggressors and the judges when it comes to recovery and disputes in the Banking sector.

On top of the 30% deposit defective unjust/unfair Regulations 13 that stands currently unconstitutional which was equally smuggled into the Ugandan laws as the mortgage act was enacted in 2010 yet Regulation 13 providing for 30% deposit was smuggled into the subsidiaries in 2012.

Banks now through (ICAMEK) want to take over the arbitration or mediation process so that customers are left with no choice but to surrender and lose their properties to the Banks. These are some of the injustices in the Banking sector for which we call for the reforms.

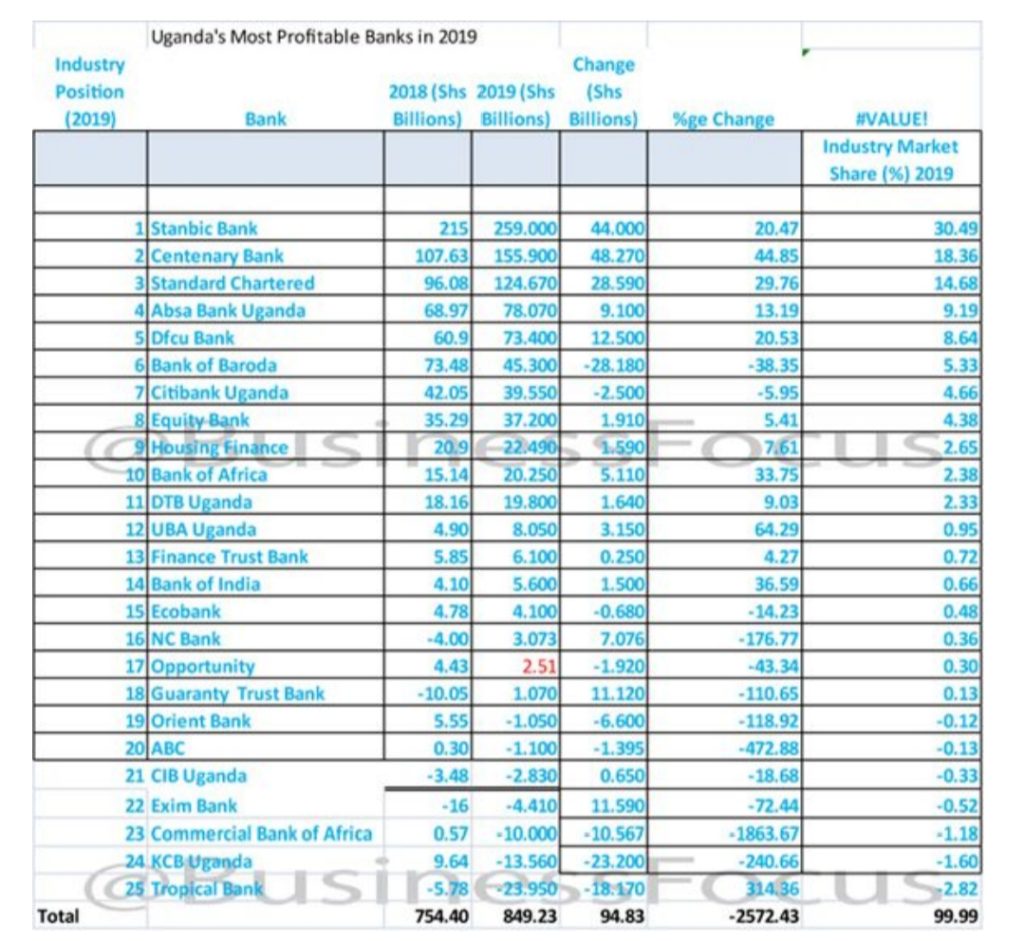

A detailed look at all Ugandan commercial banks ranked by profitability of 2019, shows that banks made total profits of Ugx- 849billion. (See table below)

A further look at the top 10 banks, they together made a profit of Ugx- 852billion and out of the top 10 banks, only 2 are Ugandan owned banks.

The remaining 8 top banks which are foreign owned together made a total profit of Ugx- 675billion in 2019. And therefore the concern is on where all this Ugx- 675billion was taken to.(Bank investors’ country of origin)

The main focus is on reason because it is the only missing factor in the reaction of the ED Uganda Bankers Association (UBA) on the proposed Banking reforms. They have written a 10 page reaction without addressing not even one of the problems. Without reason, there exists no meeting of minds. How can we possibly find a solution to a problem that the parties have either failed to understand or merely fully address their mind to? That’s why we call upon the Government to act fast and save Ugandans from these unfair current poor Banking structure that is draining all capital out of this economy under the disguise of profit repatriation.

When we talk about dominance in top management job by foreigners as opposed to Ugandans, we expect you to provide full list of all Banks, their CEOs, MDs and directors with their nationality rather than giving percentages, you should discuss matters and problems for what they really are not what you ought them to be.

When we raise the issue of discrimination as a fact avail us with all Bank loans books and we compare interest rates of Ugandans and foreigners, we compare exposure in terms of amount in loans disbursed to Ugandans as compared to foreign investors. We are discussing facts and realities on ground not drawings of financial tables and current defective policies.

About the prevailing lending rates, the average lending interest rate in the Ugandan banking industry is about 18.3% per year across all bank loan products in all customer segments.

This highly contrasts with the average deposit interest rate in the banking sector which is averaging at 9.6% per year. This presents a very huge difference between what banks pay clients who deposit funds with them and what the same banks charge people who want to borrow those deposited funds.

In the article, the ED of Uganda Bankers Association(UBA) says that one of the determinants of the very high cost of loans from commercial banks in Uganda is the cost of the funds, the above contrast goes to show that commercial banks take almost 95% markup on the funds deposited.

The concern then is to make credit as affordable/less costly as possible to enable Ugandans access more credit which then creates a spillover effect in the economy specific to the different sectors where the bank clients operate.

When we raise the issue of annual profit repatriation the answer is either yes or no, if yes as a fact we all know then why not discuss a way forward in which the two can co-exist the Banks as businesses at the same time see the best way forward on how they can reinvest the money In Uganda without affecting the customer or private sector rather than taking a defensive approach.

Uganda Bankers association (UBA) through their executive director claims to be open to suggestions that are genuine concerns however suggesting that the reforms we raised were based on falsehood packaged under the guise of nationalist sentiments then why are you panicking all over social media platforms with a defensive approach using so many economic statements and words rather than addressing the problems raised. Ugandans are not fools for whom you take us to be. It’s time we gained economic independence through Banking reforms.

The ED Uganda Bankers Association claims the Banking Sector employs 15,000 Ugandans directly yet Ham Enterprises (U) Limited to date employs directly 1,630 Ugandans as a private Limited Liability local company which is approximately 20% of the employees of all Banks in Uganda. We Bank with over 10 Banks in Uganda and hold close to 30 accounts which qualifies us to have substantial knowledge about the Ugandan Banking Sector as stakeholder. It’s in the same spirit that we call for Banking reforms for and on behalf of all Ugandans that have fallen victims of the current poor Banking structures and unfair Banking laws.

Uganda Bankers Association openly advised Ham Enterprises (U) Limited to pay up its liability with Diamond Trust Bank without addressing itself to facts of the matter before courts or taking the corporate responsibility to ask the company our side of the story as a neutral public body would have done which proves that Uganda Bankers Association are partners in crime and hold Uganda Bankers Association fully aware of all the fraud dealings in most of these Banks against their customers.

REACTIONS TO DIAMOND TRUST BANK’S SUBMISSION ON AUGUST 22, 2020 SATURDAY VISION.

Ham Enterprises (U) Limited has never denied ever acquiring loan facilities from Diamond Trust Bank however, our claim is fraud by DTB evident from our Banking statements with the Bank as well as audited books of accounts which clearly show indicate these loans were paid off and the Bank unlawfully, excessively, fraudulently debited Ugx- 34,295,951,533 from our shillings accounts and USD 23,467,670.61 from our dollar accounts a claim for which we filed a case against the Bank for recovery of the same. See attached below

Ham Enterprises (U) Limited on finding out this fraud took the responsibility and wrote to Diamond Trust Bank a letter dated 16th November 2019 issuing a termination notice of all contractual obligation with the Bank informing them of the irregularities, extortionate, unlawful, deceptive ,unauthorized transactions and debits on our accounts, the Bank had equally fraudulently through misrepresentation contracted us into unconscionable terms of contract using their superior bargaining position as a Banker unjustly jointly and severely enriching themselves. We waited for their response to that regard but received none. The silence meant the Bank was fully aware of all the fraud they had done on our accounts.

On 10th January 2020 after waiting for two months without response from the Bank we wrote a demand notice to the Bank for refund of all the monies fraudulently taken off our accounts and equally demanded for a reconciliation with a detailed explanation on why the money was debited off our accounts. We clearly requested them to refund our money within 5 working days otherwise failure of which gave us no option but to constitute legal action for recovery of the same. See attached below:

-

Termination Letter -

Demand Notice

Once we filed the case the Bank was so scared that it opted for a political approach by trying to corner the company into a position of having to first deposit 30% of whatever disputed amounts using regulation 13 which we successfully challenged claiming we were the victims here that had run to courts of law seeking justice, how then would court hold us to a condition of first paying 30% to the very Bank that had fraudulently taken money off our accounts, this was contrary, repugnant and inconsistent to article 28 which provides to right to a fair hearing and article 26 which provide for right to property as the Bank was equally trying to use this shield or defective law to take our properties against loans that were paid. We managed to fight off the defective 30% deposit under regulation 13 though we saw this as collectively unfair to all Ugandans yet so many Ugandans have lost their properties through unjust settlements forced onto them by Banks using this regulation 13 as a shield.

We decided to proceed and filled a constitutional petition No.11/2020 for and in the interest of all Ugandans because as patriotic Ugandans such unjust laws should be scrapped off our legal system hence the call to Government for Banking reforms in addition to the filled petition. See attached below.

Ham Enterprises (U) Limited has Banked with Diamond Trust Bank for approximately 10 years and the Bank claims to have extended to us a total loan facility of Ugx- 41,000,000,000 out of which they claim there is an outstanding Loan balance of Ugx- 39,700,000,000 owed to the Bank.

Ham Enterprises (U) Limited within the 10 year Banking relationship with Diamond Trust Bank on record and company statement has paid total interest of Ugx- 22,005,452,398 and Total Principle of Ugx – 23,529,913,107 making a total Payment of Ugx- 45,535,365,505 monies directly paid to the Bank, does it imply that we have simply been donating or giving charity for these loans to have reduced by only approximately Ugx- 2,000,000,000 out of the Ugx- 45,535,365,505 we have so far paid to the Bank. With all we have paid to this Bank how can a mere ED of Uganda Bankers Association afford to insult us by calling us “bad borrowers”. Our claim is not only limited to the Ugx- 45,535,365,505 paid but rather on a total of Ugx-120Billion unlawfully, irregularly, unexplained and un authorized debits off our accounts in a period of 10 years.

Majority of these Ugandan foreign Banks come to Uganda disguising as big investors with substantial capital yet it’s all fictitious. They use our deposits and savings as the core base of their operational capital yet undermining us patriotic Ugandans that fight so hard for the economy to thrive and aim at seeing that our motherland Uganda develops.

Diamond Trust Bank Uganda is 3 to 4 times smaller than Ham Enterprises (U) Limited as a private local company. Diamond Trust Bank was founded in 1945 as Diamond Jubilee Investment Trust (DJIT) to extend credit to the East African Ismaili’s community, in 1968 it upgraded to Diamond Trust Properties Uganda Limited, in 1972 it commenced operation as an non Banking Financial Institution as Diamond Trust Bank Uganda Limited (DTBU). It’s in 1995 that the Institution was recapitalized by Agha Khan Fund for economic development and in 1997, the bank became a fully serviced commercial bank; Diamond Trust Bank Uganda Limited.

Diamond Trust Bank Uganda has been operational in Uganda for 75 years now but it has never had a Ugandan Managing Director and as of December 2018, the total Bank assets were valued at Ugx- 1.606 Trillion out of which Ugx- 1.2 Trillion are customer’s deposits leaving a balance of approximately Ugx- 400 billion inclusive of all their liabilities, premises including head offices buildings, every small thing they own including computers, furniture and security deposit with Bank of Uganda.

So minus all these from the Ugx-400billion, the Bank is left with less than Ugx-100 billion as capital; yet we have raised a case against this same bank for recovery of Ugx- 120 billion which leaves us wondering that with all the conclusive evidence filed in court, if courts of law determine that the Bank should pay us, where does it leave the Bank?

As Ugandans we should stop looking at ourselves from an inferiority point of view and stand strong against such oppression in our motherland Uganda. We should equally stop looking at foreigners as semi gods, they are not better than us. We should stand strong for our nation and call for Banking reforms and other reforms in all sectors where we see problems in the interest of development of our country Uganda.

Based on reason and reality there are limited resources available to satisfy every man’s unlimited wants, one’s ability to exploit and explore the available limited resources enables them to out compete others hence becoming the determinant factor between success and failure between individuals, societies or nations. These current policies in our Banking sector are one of the major reasons why Uganda is failing as a country at large.

Let courts of law first determine the case we filed against the Bank for recovery of our money.

Then we shall proceed to file cases against individuals, holding them accountable for the fraudulent and money laundering acts that caused unlawful debits of money from our accounts, good enough; Ham Enterprises (U) Ltd being a high profile client only dealt with top management with both DTB Uganda / DTB Kenya.

These people take us all Ugandans for granted and always tend to undermine our reasoning capacity.

We equally bring it to the attention of all Ugandans that we have fully facilitated the registration of Uganda Borrowers Association and Uganda Bank Consumers Association. whose major role is to stand for the rights of all Ugandans that have fallen victims of this poor Banking structures including to mention but a few;

- Legal representation of all Bank customers that have unjustly been affected by fraud in Banks.

- Push for Banking reforms.

- Call for setting aside and retrial of all past judgment/settlements that were unjustly/unfairly settled with loss of property as a result of the defective 30% deposit Regulation 13. We have equally already filed a petition at constitutional court against the unconstitutionality of regulation 13

- Offer free legal representation to all clients in regard to all fraud cases in Diamond Trust Bank.

- Investigate fraud against customers in Banks and offer solutions to related Banking problems that customers face.

- Advise Government or give opinions on Banking related issues like;

●Reforms in Bank of Uganda management and operational structures as a regulator i.e. like the current fact that the Governor Bank of Uganda is the Chairman of the Board that is supposed to supervise the operation of Bank of Uganda and others.

●The ED of Uganda Bankers Association further notes that in Uganda, one third(1/3)of total industry deposits(which is Ugx 24trillion)is invested in treasury bills, which means that only Ugx- 16 trillion is left for borrowers to apply for, both individuals and non-individuals. This would definitely make the cost of loans high, given that the demand is very high yet the supply is low.

●The ED of Uganda Borrowers Association himself confirmed in the new vision publication of 29 June 2017 that this government borrowing worsens the loan interest rates making borrowing very expensive for the private sector.

As at end June 2019, commercial banks in the country accounted for 95.2% of the banking sector total assets of Shs31.8 trillion as the banking industry aggregate assets increased by 10.5 percent to Shs30.3 trillion from Shs 27.4 trillion in June 2018, according to the financial stability report for June 2019 as released by the Bank of Uganda (BOU).

●This goes to show that the aggregate demand for loans in the industry just keeps increasing, and therefore this has to be matched by availability of cheap deposits. But this can’t be possible if commercial banks keep putting a third (1/3)of the deposits in treasury bills

●Mismanagement of commercial Banks by the regulator. The law requires commercial banks to give Ugx-25 billion as security deposit to the Bank of Uganda and are equally required to keep 25% of their capital with the Bank of Uganda. How then do we have many Banks collapsing randomly.

- Monitor interest rates or advocate for capping of interest rates like it was done in Kenya.

- Represent customers of the Banks in formulation of policies, laws, structures at all levels in Government just like the Uganda Bankers Association does.

- As stakeholders and employers of the Banks; keep track of all banking activities and intentions towards our customers to ensure fairness and transparency in the banks’ day to day operations.

- Protect national interests when it comes to Banking and avoid extortion/exploitation as it stands as a fact that there exist acts of Tax evasion/avoidance by Banks and money laundering. We intend to raise this with the Government and file cases in courts of law to that regard.

- Ensure reduction in bad loans as a result of poor Banking structures and policies that have frustrated the ability of Ugandan borrowers to pay back loans hence losing their properties, Why do Ugandans come to banks rich with properties they pledge as securities and leave poor? Does it imply that all Ugandans are poor business Managers? Or the problem is with the System?

In line with the need for specific/sustained stimuli like guarantee frameworks to mitigate risks in specific sectors, it’s not that they are lacking, but little has been done by commercial banks to notify the public about their availability.

Specifically to the highest risk sector which is agriculture, there are different guarantee schemes available but there is little knowledge available to the borrowers.

For example, The Agricultural Credit Facility (ACF) was set up by the Government of Uganda (GoU) in partnership with Commercial Banks, Uganda Development Bank Ltd (UDBL), Micro Deposit Taking Institutions (MDIs) and Credit Institutions all referred to as Participating Financial Institutions (PFIs). The Scheme’s operations started in October 2009, with the aim of facilitating the provision of medium and long term financing to projects engaged in Agriculture and Agro processing, focusing mainly on commercialization and value addition. The ACF has a fixed interest rate of 12% per year.

There are other guarantee schemes like the ABI Finance scheme which covers up to 50% of the loan amount for all loans in the agricultural value chain.

When it comes to big loans why do Banks prefer raising money from their branches/partners abroad that are not registered in Uganda rather than recapitalize their Banks on ground? It’s illegal, amounts to money laundering and they do so because they don’t want to pay taxes to the Government on these loans so Uganda is fully extorted/exploited and used as a mere conduit for the progress of other economies.

- The other issue is with loan insurance, clients are required to insure them e.g. Personal loans and mortgaged/homes loans are insured against death and permanent disability.

When a client passes away or gets an accident that stops them from active work, the insurance company is supposed to pay off that loan, but for many banks; client’s families are forced to continue paying even when the insurance company has paid up the loan. When the families claim for what they paid, the banks do not refund.

The Banking sector in Uganda thrives at the cost of all other sectors however the reasonable thing to do is to open our minds to the problems raised and forge a way forward in the interest of the development of our motherland Uganda.

A call for Banking reforms and independence of our economy and development of our motherland Uganda should be received with open hearts. Whoever receives this in a bad spirit is not even patriotic enough to be called a Ugandan, for God and My Country.

It’s very disheartening that through the Uganda Bankers Association these Banks use fellow Ugandans to fully exploit our lovely country. Depriving us of all our would be development capital keeping us in a constant state of economic dependency yet you still retrain and desist from opening up your minds to actual realistic facts and problems in the Banking sector that have kept this economy on its knees since the colonial times.

- The ED Uganda Bankers Association is a former Managing director and chief executive officer of United Bank for Africa in Uganda) for 3 years and before that he was the Head of retail banking at DFCU Bank, Head of channels at Barclays Bank of Uganda, Financial controller at Sara Lee (East Africa) and the Head of budget at Colgate Palmolive (East Africa). It is therefore not surprising that his response is merely defensive in nature instead of having an open mind to receive the suggestions for the needed changes in the banking industry. From the above this proves that Wilbrod Humphreys is part of the problem himself, so how do you expect him to give us a solution?

It’s in my opinion that this is a disservice to your motherland, our lovely country Uganda.

I call upon the Government to call for a platform for all stakeholders in the Banking industries like the Banks, Uganda Bankers Association, Uganda Borrowers’ Association ,Bank of Uganda, representation from the judiciary, Members of Parliament, Ministry of Finance and representation of us the customers (Ugandans) being the major stakeholders. With open minds, and soft hearts, to fully discuss the problem and possible way forward because at the rate foreign Banks are exploiting the economy we shall be reduced to mere spectators with zero ownership or say very soon.

We humbly call and seek for Banking reforms to this regard.

Mr. Kiggundu Hamis is the C.E.O/ Managing Director of Ham Group of Companies, popularly trading as Ham Enterprises (U) Limited, a general conglomerate in Uganda directly employing about 1630 people.

Would you like to get published on this Website? You can now email Daily Post Uganda: an Opinion, any breaking news, Exposes, story ideas, human interest articles or interesting videos on: dailypostug@gmail.com Videos and pictures can be sent to +256 702879647 on WhatsApp